How to Manage Retirement Savings When Interest Rates Stay Elevated

The definitive guide for investors who want to protect and grow their nest‑egg in a high‑rate world

Table of Contents

- Why Interest Rates Matter for Retirement

- What “Elevated” Really Means – The Current Landscape

- Core Principles for a High‑Rate Retirement Plan

- Tactical Tools & Asset Classes

-

- 4.1. Fixed‑Income Strategies

- 4.2. Cash‑Equivalent Vehicles

- 4.3. Equities & Dividend Playbooks

- 4.4. Real Assets & Inflation Hedges

- 4.5. Annuities and Income Guarantees

- Tax‑Efficient Maneuvers in a Rising‑Rate World

- Rebalancing, Risk Management, and the “Liquidity Buffer”

- Behavioral Finance: Keeping Emotions in Check

- Action‑Oriented Checklist

- Looking Ahead – Scenario Planning

- Final Thoughts

- Why Interest Rates Matter for Retirement

Interest rates are the quiet, invisible hand that moves almost every corner of the financial market. For retirees and those approaching retirement, interest rates shape three fundamental aspects of a portfolio:

- Income Generation – The coupon on a bond, the dividend yield on a stock, or the payout from a bank account all respond to the prevailing rate environment.

- Purchasing Power – Higher rates usually accompany higher inflation, eroding the real value of cash and fixed‑income returns.

- Opportunity Cost – If you park money in a low‑yield savings account while Treasury yields climb, you’re effectively “paying yourself” for not taking advantage of higher returns elsewhere.

When rates stay elevated for an extended period, the old “safe‑as‑cash” retirement strategy (i.e., large cash cushions and short‑duration bonds) can become a drag on performance. The challenge is to balance safety with growth while protecting against inflation and preserving liquidity for unexpected expenses.

- What “Elevated” Really Means – The Current Landscape

Data snapshot (as of early 2024)

- U.S. 10‑Year Treasury Yield: ~4.3%

- Fed Funds Rate: 5.25%–5.50% (the highest in 22 years)

- Core CPI YoY: 3.2% (still above the long‑run target of 2%)

- High‑Yield Savings Accounts: 4.0%–4.75% APY

These numbers tell a clear story: the cost of borrowing is up, but so are the rates you can earn on relatively safe assets. However, “elevated” does not mean “permanent.” Central banks have signaled a gradual easing over the next 12–18 months, while inflation pressures remain uneven across sectors.

Key take‑aways for retirees

| Factor | Effect on Retirement Portfolio | What to Watch |

| Higher nominal yields | More income from bonds, CDs, and high‑yield savings | Duration risk – longer‑dated bonds may lose value if rates fall |

| Elevated inflation | Real returns on cash and nominal bonds can be negative | Inflation‑linked securities (TIPS, I‑bonds) |

| Volatility in equity markets | Risk‑premium may rise as investors price in rate uncertainty | Dividend‑focused equities and defensive sectors |

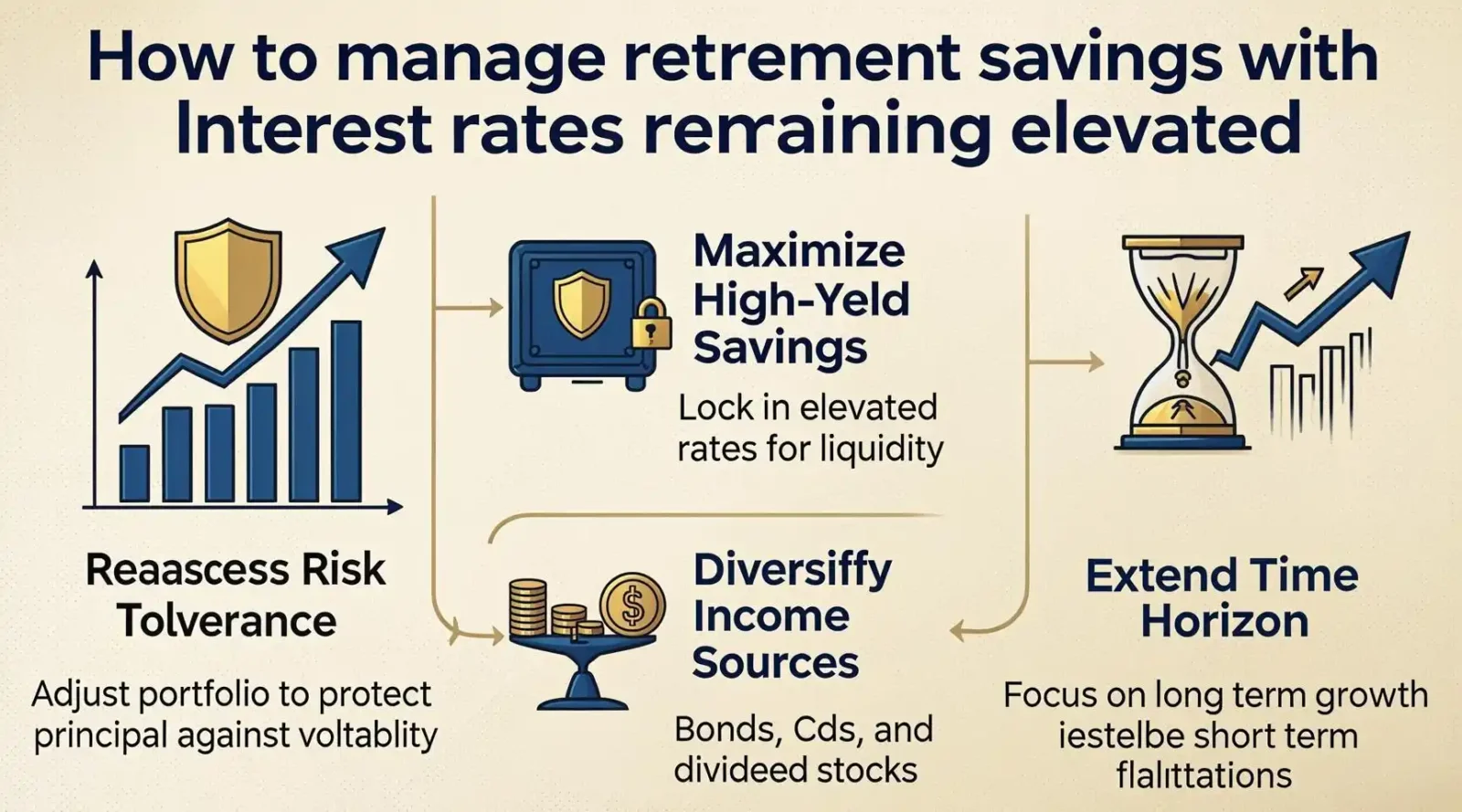

- Core Principles for a High‑Rate Retirement Plan

Even with the market’s shifting sands, a solid strategic backbone remains unchanged. These five principles should guide every decision:

- Diversify Across Yield Sources – Combine bonds, cash equivalents, dividend stocks, and real assets so you’re not dependent on a single income stream.

- Match Duration with Time Horizon – Use shorter‑duration bonds for nearer‑term cash needs and longer‑duration, higher‑yielding bonds for the “stable‑income” portion of the portfolio.

- Preserve Inflation‑Adjusted Purchasing Power – Allocate a meaningful slice to inflation‑protected instruments (e.g., TIPS, I‑bonds, real‑estate).

- Maintain a Liquidity Buffer – Keep 6–12 months of living expenses in highly liquid, FDIC‑insured accounts to avoid forced sales during market dips.

- Stay Tax‑Efficient – Place taxable high‑yield assets in tax‑advantaged accounts where possible, and use tax‑loss harvesting to offset ordinary income.

- Tactical Tools & Asset Classes

Below we break down the specific vehicles that thrive—or at least survive—when interest rates remain elevated. Each subsection includes a practical “how‑to” for implementation.

4.1. Fixed‑Income Strategies

| Strategy | Why It Works in a High‑Rate World | Potential Pitfalls | Implementation Tips |

| Short‑Duration Bond Funds (1–3 yr) | Minimal price volatility; can be reinvested at higher yields as old bonds mature. | Lower yields than long‑duration bonds. | Use funds like Vanguard Short‑Term Treasury Index (VGSH) or a municipal equivalent for tax‑free income. |

| Laddered CDs | Guarantees a rising rate floor—each CD matures at a higher yield as rates climb. | Early withdrawal penalties. | Build a 5‑year ladder (e.g., 1‑yr, 2‑yr, … 5‑yr) using broker‑deposited CDs for flexibility. |

| Corporate Bond ETFs with “Barbell” Tilt | Combine high‑quality short‑term bonds with selective long‑term “high‑coupon” issues to capture yield while limiting duration risk. | Credit risk if you stray into lower‑grade corporates. | Consider iShares Short Treasury (SHV) + iShares 10‑Year Treasury (TLH) or SPDR Bloomberg High Yield Bond (JNK) for a modest risk‑adjusted profile. |

| Floating‑Rate Notes (FRNs) | Coupon resets periodically, keeping pace with short‑term rates; immune to falling bond prices when rates rise. | Generally low yields in a flat environment; may under‑perform when rates plateau. | Look at iShares Floating Rate Bond ETF (FLOT) or directly purchase Treasury FRNs via TreasuryDirect. |

| Treasury Inflation‑Protected Securities (TIPS) | Principal adjusts with CPI, safeguarding real purchasing power. | Real yields can be negative when inflation expectations are low. | Use Vanguard Short‑Term TIPS (VTIP) for liquidity and lower duration. |

Practical Example – Building a Fixed‑Income Core (Age 68)

| Allocation | Product | Rationale |

| 30% | Short‑Duration Treasury ETF (e.g., VGSH) | Stable, low‑risk base; quick turnover. |

| 20% | Laddered CDs (1‑5 yrs) | Guaranteed rates, predictable cash flow. |

| 20% | High‑Yield Corporate Bond ETF (JNK) | Extra yield; allocate within taxable bucket. |

| 15% | TIPS (VTIP) | Inflation shield for core purchasing power. |

| 15% | Floating‑Rate Note ETF (FLOT) | Rate‑sensitive income, low price volatility. |

Total: 100% of the fixed‑income slice, delivering an effective yield of 3.8%–4.2% before taxes.

4.2. Cash‑Equivalent Vehicles

Even in a rising‑rate climate, cash still has a place—especially for emergency liquidity and short‑term spending windows.

| Vehicle | Current APY (2024) | FDIC/Insurance | Ideal Use |

| High‑Yield Online Savings | 4.00%–4.75% | Up to $250k per depositor, per bank | 6‑month “buffer” + discretionary spend |

| Money‑Market Mutual Funds | 3.70%–4.20% | SIPC protects securities, not deposits | Bridge funding between CD maturities |

| Cash‑Secured Put Strategies (via brokerage) | Variable; can exceed 5% in premium | Requires margin; not FDIC‑insured | Generates extra yield on cash you intend to keep in the market |

Tip: Keep the high‑yield savings accounts spread across two FDIC‑insured banks to stay under the $250k per institution limit while maximizing the overall APY.

4.3. Equities & Dividend Playbooks

Stocks might seem at odds with “high rates,” but selective equity exposure can still deliver growth and income.

| Equity Focus | Why It Works in a High‑Rate World | Example ETFs/Funds |

| Dividend Aristocrats (30+ years of increasing dividends) | Companies with stable cash flows tend to retain earnings even when financing costs rise. | SPDR S&P Dividend (SDY), Vanguard Dividend Appreciation (VIG) |

| Utilities & Consumer Staples (Defensive sectors) | Earnings are less cyclical; utilities often benefit from rate‑linked regulated returns. | Utilities Select Sector SPDR (XLU), Consumer Staples Select Sector (XLP) |

| REITs with Short‑Term Leases | Some REITs can pass higher borrowing costs onto tenants via lease escalations. | Realty Income (O), Crown Castle (CCI) – but watch interest‑rate sensitivity. |

| Low‑Beta, High‑Quality Large‑Cap | Lower volatility, smoother earnings; can hold steady while bonds adjust. | iShares Edge MSCI Min Vol USA (USMV) |

Dividend Yield Strategy Checklist

- Screen for >3% dividend yield and a pay‑out ratio <60%.

- Confirm a 5‑year dividend growth rate >5% (shows sustainability).

- Check forward earnings estimates to ensure cash flow can cover dividends in a higher‑rate environment.

A well‑balanced equity‑income slice typically makes up 15%–25% of a retiree’s total portfolio, depending on risk tolerance.

4.4. Real Assets & Inflation Hedges

When inflation and rates move together, real assets can provide a “double‑dip” protection.

| Asset | Inflation‑Link | Rate Sensitivity | How to Access |

| Real Estate (REITs) | Rental contracts often include CPI escalators. | Moderate—interest rates affect cap rates. | Direct REITs, open‑ended REIT ETFs. |

| Commodities (Gold, Energy) | Gold historically preserves value in high‑inflation periods. | Low correlation with bonds; can offset rate moves. | Commodity ETFs (GLD, UUP) or futures for advanced investors. |

| Infrastructure Funds | Long‑term contracts tied to inflation (e.g., toll roads). | Low—stable cash flows. | iShares Global Infrastructure (IGF), Alerian MLP ETF (AMLP) (note tax considerations). |

| Private Debt / Direct Lending | Loans issued at floating rates, often with spread over LIBOR/SOFR. | Sensitive to rate changes but generate higher yields. | Usually accessed via specialized platforms or closed‑ended funds. |

Practical Allocation (Age 72, Moderate Risk)

- 8% REITs (focus on dividend‑heavy, short‑lease properties).

- 4% Gold/Precious Metals (via physical‑backed ETFs).

- 3% Infrastructure (global exposure).

Total 15% of total assets, but only 5%–7% of the risk‑adjusted portion due to lower volatility.

4.5. Annuities and Income Guarantees

Annuities can lock in a real, inflation‑adjusted income stream—a valuable hedge when rates are high.

| Annuity Type | Rate Environment Fit | Key Feature | Typical Cost |

| Immediate Fixed Annuity with Inflation Rider | Higher starting payout because rates are high. | Guarantees a base income plus CPI increase. | 1%–2% of premium per year (administrative). |

| Deferred Fixed Annuity (Multi‑Year) | Lock in today’s elevated rates for future payouts. | Higher credited interest for the deferral period. | Similar to immediate; surrender charges if cashed early. |

| Variable Annuity with Income Rider | Allows market participation while locking a floor. | Income floor based on a % of premium; upside participation. | Often >3% of premium, plus underlying fund expenses. |

When to Consider:

If you have already covered essential expenses with a diversified portfolio, an annuity can cover non‑essential discretionary spend (travel, hobbies) and act as a “longevity insurance.”

Caution: Avoid over‑allocating to annuities; they are illiquid and come with fees that can erode returns if you need the capital for emergencies.

- Tax‑Efficient Maneuvers in a Rising‑Rate World

High yields often come with high ordinary‑income taxes. Here’s how to keep Uncle Sam from eating your gains:

| Income Source | Tax Treatment | Optimization Strategies |

| Interest from Savings / CDs | Ordinary income | Place in Roth IRA (if eligible) or Traditional IRA to defer taxes; otherwise use tax‑advantaged health savings accounts (HSAs) for those over 65. |

| Bond Interest (Treasury, Municipals) | Treasury: Federal tax; Municipal: Federal tax‑exempt, sometimes state‑exempt. | Municipal bond ETFs for high‑tax‑bracket retirees; hold Treasury bonds in a Roth if you anticipate higher future tax rates. |

| Qualified Dividends | 0%‑20% (depends on income) | Use qualified‑dividend ETFs inside taxable accounts; keep them out of traditional IRAs where they become ordinary income. |

| Capital Gains (Equities, REITs) | 0%‑20% + 3.8% Net Investment Income Tax (NIIT) if AGI > $200k (single) | Tax‑loss harvesting each year; consider strategic rebalancing to realize gains in low‑income years (e.g., early retirement). |

| Annuity Income | Ordinary income (except for non‑qualified principal) | Use annuity ladder and partial Roth conversions to spread tax liability over several years. |

The “Tax‑Bracket Smoothing” Technique

- Estimate your AGI for the upcoming year (including Social Security, pensions, investment income).

- Project the tax bracket you’ll fall into.

- Allocate high‑interest, taxable assets (e.g., high‑yield CDs) to tax‑deferred accounts to keep AGI below the NIIT threshold.

- Shift qualified‑dividend or capital‑gain producing assets (e.g., stocks) into taxable accounts when you’re already in a lower bracket.

- Rebalancing, Risk Management, and the “Liquidity Buffer”

6.1. Rebalancing Frequency

- Quarterly: If you’re heavily exposed to rate‑sensitive assets (e.g., floating‑rate notes), a quarterly review keeps the portfolio aligned with target allocations.

- Semi‑Annual: Most retirees find a twice‑yearly rebalance sufficient for stable, diversified allocations.

Rule of Thumb: If any asset class drifts >5% from its target, trigger a rebalance.

6.2. Managing Duration Risk

- Duration Gap: Aim for a duration gap (difference between the duration of assets and the duration of liabilities) near zero for retirees who rely on portfolio income for living expenses.

- Tools: Use online bond calculators or your brokerage’s “duration” metric to measure the overall sensitivity of your fixed‑income holdings.

6.3. Building the Liquidity Buffer

| Buffer Tier | Instrument | Yield (2024) | Access Time |

| Tier 1 – Immediate | FDIC‑insured high‑yield savings | 4.0%–4.75% | Anytime |

| Tier 2 – Near‑Term | 1‑year CD ladder | 4.5% | 30–90 days notice (if using brokered CDs) |

| Tier 3 – Short‑Term | Money‑Market ETFs | 3.7%–4.2% | Same‑day trade settlement |

Guideline: Keep 6–12 months of essential expenses in Tier 1+2 combined. Anything beyond that can be deployed into higher‑yield or growth‑oriented vehicles.

- Behavioral Finance: Keeping Emotions in Check

Even the most sophisticated plan can crumble if fear or greed drive decisions. High‑rate periods often bring media hype around “bond busts” or “rate peaks.”

Three Psychological Traps & Counter‑Measures

| Trap | Description | Counter‑Measure |

| Loss Aversion | Over‑reacting to temporary dips in bond prices. | Use bond ladders; each rung matures at a higher yield, providing a visual proof of progress. |

| Recency Bias | Assuming the current rate environment will continue indefinitely. | Conduct annual scenario analysis (rates falling, staying high, or rising further). |

| Over‑Concentration | Chasing the highest‑yielding asset (e.g., high‑yield corporate bonds) without regard to credit risk. | Stick to a pre‑defined credit‑quality filter (e.g., BBB‑or‑higher) and diversify across sectors. |

Practical Exercise: Write a “Rate‑Risk Journal”—once a month, note the headline, your emotional reaction, and the specific action (or inaction) you took. Review after six months to see whether you moved in line with your plan.

- Action‑Oriented Checklist

| ✅ | Item | Why It Matters |

| 1 | Assess Current Income Needs – calculate essential vs. discretionary cash flow. | Determines size of liquidity buffer & safe‑draw rate. |

| 2 | Audit Existing Fixed‑Income Holdings – note duration, credit quality, and tax status. | Identifies over‑exposure to long‑duration bonds that could under‑perform. |

| 3 | Open/Consolidate High‑Yield Savings – ensure FDIC coverage across multiple banks. | Locks in the current elevated rates for cash. |

| 4 | Build a Bond Ladder – e.g., 1‑yr, 2‑yr, 3‑yr, 5‑yr CDs or Treasury notes. | Provides a rising‑rate floor and predictable cash flow. |

| 5 | Add Inflation‑Protected Securities – TIPS or I‑bonds up to 25% of fixed‑income core. | Safeguards purchasing power. |

| 6 | Allocate 15%‑25% to Dividend‑Yielding Equities – prioritize Aristocrats and low‑beta large caps. | Generates growth + income, diversifies away from pure fixed income. |

| 7 | Introduce Real‑Asset Exposure – REITs, commodities, infrastructure ETFs. | Adds inflation hedge and reduces correlation with bonds. |

| 8 | Consider a Modest Annuity (5%–10% of portfolio) with an inflation rider. | Provides guaranteed income and longevity insurance. |

| 9 | Tax‑Optimize – move high‑interest taxable assets into IRA/ROTH where possible. | Lowers net‑of‑tax returns. |

| 10 | Set Rebalancing Alerts – 5% drift threshold, quarterly review. | Keeps risk/return profile on target. |

| 11 | Document Emotional Triggers – maintain a rate‑risk journal. | Improves discipline & reduces impulsive moves. |

Implementation Timeline (First Six Months)

| Month | Primary Focus |

| 1 | Complete cash‑flow analysis & set up high‑yield savings accounts. |

| 2 | Build a 1‑yr and 2‑yr CD ladder; evaluate existing bond holdings. |

| 3 | Purchase TIPS/TIP ETFs and a short‑duration bond fund to replace high‑risk long bonds. |

| 4 | Add dividend‑focused equity ETFs; rebalance to target percentages. |

| 5 | Allocate to REITs & commodity ETFs; review tax implications. |

| 6 | Evaluate annuity quotes; decide on a small fixed‑income annuity with inflation rider. |

- Looking Ahead – Scenario Planning

Because interest rates are a moving target, preparing for multiple futures is prudent. Below are three plausible scenarios and suggested portfolio tweaks.

| Scenario | Rate Trend | Inflation Outlook | Recommended Adjustments |

| A. Rate Decline (Next 12–18 months) | Fed cuts 0.5%‑1% per quarter | Moderate, trending down to 2% | Shift a portion of the ladder to longer‑duration bonds (5‑yr Treasury) to lock in higher yields before they fall. Consider bond‑funds with a “barbell” strategy for yield capture. |

| B. Rate Plateau (Steady 5%‑5.5%) | No major cuts; rates stay high | Inflation slowly declines to 2.5% | Maintain current “high‑yield” allocation; increase floating‑rate notes for rate protection. Keep inflation‑linked assets modest (10%–15%). |

| C. Rate Spike (Unexpected jump to 6%+) | Fed hikes due to renewed inflation pressure | Inflation spikes to >4% | Accelerate ladder building: lock in longer CD terms now; add short‑duration, high‑coupon corporates; boost real‑asset exposure (especially commodities). Use inflation‑adjusted annuity riders to lock in a real income floor. |

Tip: Run a simple spreadsheet that updates the projected cash flows with each scenario. The “what‑if” numbers will guide you on whether you need to increase liquidity (Scenario C) or capture yield (Scenario A).

- Final Thoughts

Retirement in an environment of elevated interest rates is not a death knell—it is a new set of tools for savvy savers. By:

- Diversifying across fixed‑income, equities, real assets, and annuity products,

- Protecting purchasing power with inflation‑linked securities,

- Keeping a liquidity buffer that earns a market‑competitive rate, and

- Managing taxes and rebalancing with disciplined processes,

you can turn the current rate regime into a steady income engine while preserving growth potential for the decades ahead.

Remember: A plan is only as good as the person who follows it. Use the checklists, stay aware of behavioral pitfalls, and revisit your assumptions at least twice a year. With the right framework, high rates become a friend rather than a foe — delivering the financial freedom you’ve worked so hard to achieve.

🔑 Quick Recap

| Core Pillar | Action | Expected Benefit |

| Yield | Laddered CDs, short‑duration bond ETFs, FRNs | Higher, predictable cash flow |

| Inflation Protection | TIPS, dividend aristocrats, REITs | Preserve real spending power |

| Liquidity | High‑yield savings, money‑market funds | Avoid forced sales, maintain flexibility |

| Tax Efficiency | Place high‑interest assets in IRAs/HSAs | Keep more of your earnings |

| Behavioral Discipline | Rate‑risk journal, set drift thresholds | Reduce emotional decision‑making |

Disclaimer

The information provided in this article is for general educational purposes only and does not constitute professional financial, tax, or legal advice. Investment decisions should be based on an individual’s personal circumstances, risk tolerance, and financial goals. Readers are encouraged to consult with a qualified financial advisor, tax professional, or attorney before implementing any of the strategies discussed herein.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment